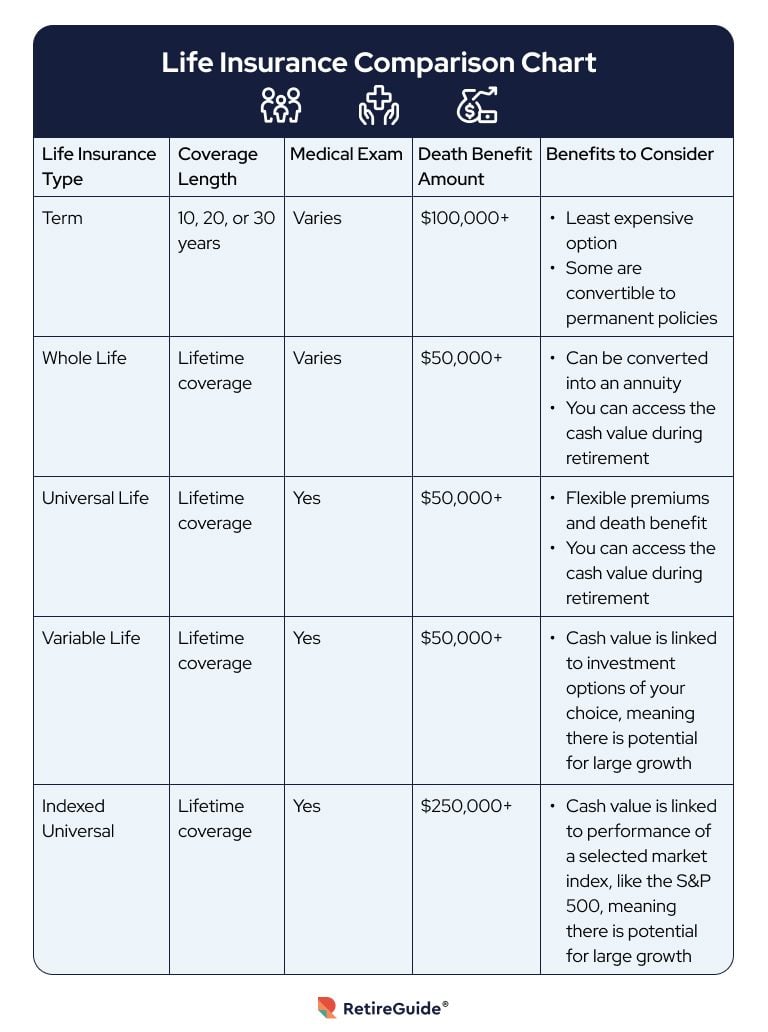

Understanding the Key Differences: Term vs. Whole Life Insurance

When it comes to choosing the right life insurance policy, understanding the key differences between term life insurance and whole life insurance is crucial. Term life insurance provides coverage for a specified period, typically ranging from 10 to 30 years. If the insured individual passes away during this term, the beneficiaries receive a death benefit. However, once the term expires, the coverage ends, and there is no cash value accumulated. This makes term life insurance generally more affordable and appealing for those seeking temporary coverage, such as young families needing financial protection while raising children.

On the other hand, whole life insurance offers permanent coverage, lasting for the insured's entire life as long as premiums are paid. In addition to a death benefit, it also accumulates cash value over time, which can be borrowed against or surrendered if needed. This dual benefit makes whole life insurance more expensive than term policies. However, for individuals seeking long-term financial security and investment opportunities, the stability and savings component of whole life insurance can be quite attractive. Ultimately, the choice between these two types of coverage should align with one’s personal financial goals and circumstances.

Top 5 Factors to Consider When Choosing an Insurance Policy

Choosing the right insurance policy can be a daunting task, especially given the myriad of options available. One of the top factors to consider is the type of coverage needed. Assessing your personal situation, including assets, liabilities, and potential risks, can help you determine the appropriate coverage. For example, health insurance may differ vastly from auto insurance, with each having its unique requirements and benefits. Understanding your needs is crucial in navigating through different policies effectively.

Another important consideration is the policy premium and deductible. Typically, lower premiums may seem appealing, but they often come with higher deductibles, which can lead to unexpected expenses in the event of a claim. It's essential to calculate the total cost of the policy over time and balance it against the benefits offered. Additionally, reviewing customer ratings and claim settlement ratios can provide insights into the insurer's reliability and customer service, further guiding your decision.

Is Your Insurance Policy Delivering Enough Value?

When assessing whether your insurance policy is delivering enough value, it's crucial to review the coverage options that are included. Many people overlook the specifics of their policies, which can lead to gaps in coverage or excessive payments for services they don't need. Begin by making a list of your current coverage and compare it with typical needs for your situation. For instance, consider whether you have adequate liability coverage or if you're underinsured against natural disasters. It might be beneficial to consult with an insurance agent to identify any unnecessary riders that could be removed from your policy.

Another important aspect is to evaluate the claims process and customer service of your insurance provider. Insurance policies can be challenging to navigate, and having responsive support when you need to make a claim is invaluable. Look for reviews or testimonials about your provider's claims process, as this can indicate the real-world value of your policy. If you find that the support is lacking or reviews are predominantly negative, it may be time to consider switching providers to ensure you're getting the best value for your investment.