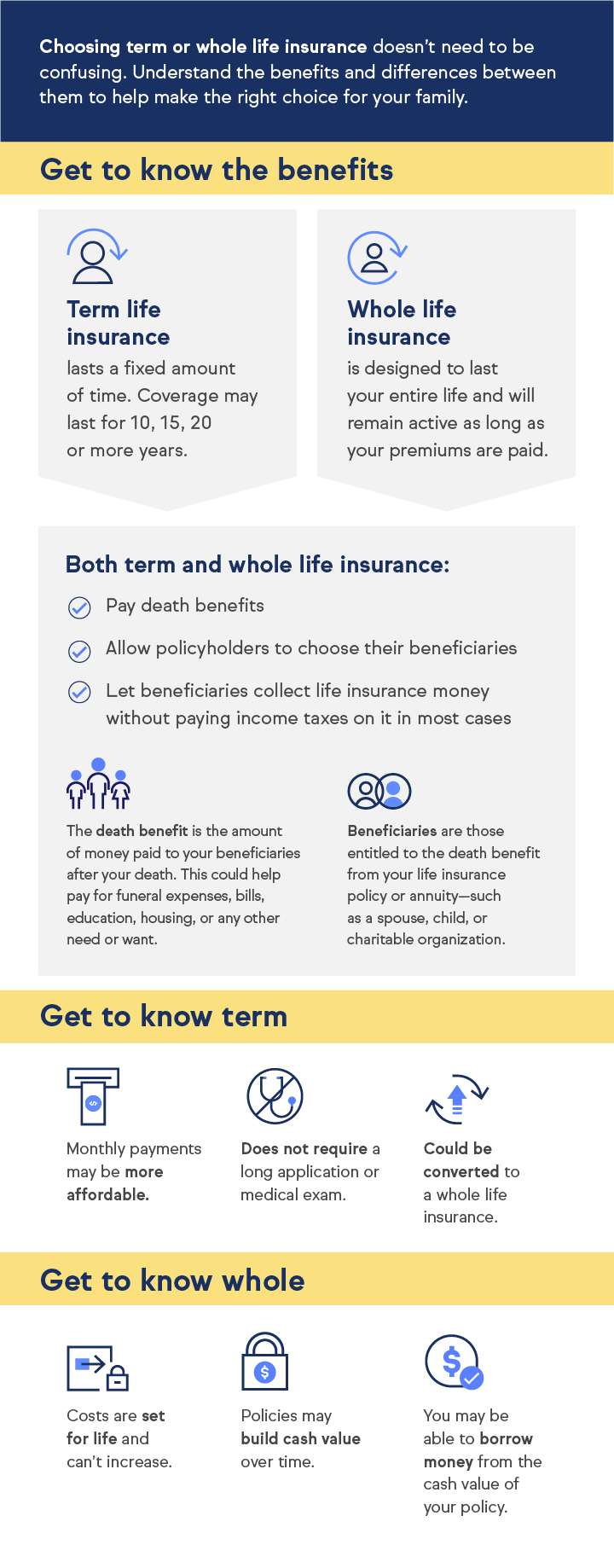

What is Term Life Insurance and How Does It Work?

Term life insurance is a type of life insurance policy that provides coverage for a specified period, known as the term. Typically, these terms can range from 10 to 30 years. If the insured passes away during this term, their beneficiaries receive a death benefit, which is a tax-free lump sum that can help cover living expenses, debts, and other financial obligations. This makes term life insurance an attractive option for young families and individuals who want to ensure financial security for their loved ones without incurring high premiums associated with whole life policies.

The mechanics of how term life insurance works are relatively straightforward. When you purchase a policy, you choose the duration of coverage and the benefit amount. You then pay regular premiums, which are typically lower than those of permanent life insurance options. If you outlive the policy term, the coverage ends, and no payout is made. However, many policies offer a renewal option or a conversion to a permanent policy, allowing policyholders to maintain life insurance coverage even after the term expires, although at potentially higher rates. Understanding term life insurance helps individuals make informed decisions about their financial planning and insurance needs.

Top 5 Reasons to Consider Term Life Insurance for Your Family

When it comes to securing your family's financial future, term life insurance offers an affordable solution that can provide peace of mind. Here are the top 5 reasons to consider this essential coverage:

- Affordability: Term life insurance premiums are generally lower compared to whole life policies, making it an accessible option for families looking to protect their loved ones without breaking the bank.

- Temporary Coverage: This type of insurance is ideal for families who need coverage for a specific period, such as until the children are financially independent or the mortgage is paid off.

Additionally, term life insurance provides a straightforward and transparent coverage option. Here are three more compelling reasons:

- Flexibility: Policyholders can choose the length of the term, typically ranging from 10 to 30 years, allowing them to tailor coverage to their family's evolving needs.

- Simple Payouts: In the event of the policyholder's passing, the beneficiaries receive a lump sum payout, which can be used for various expenses, including daily living costs, education, and debt repayment.

- Peace of Mind: Knowing that your family is financially protected provides a sense of security, allowing you to focus on the present while planning for the future.

How to Choose the Right Term Life Insurance Policy for Your Needs

Choosing the right term life insurance policy is crucial for ensuring that your loved ones are financially protected in case of unexpected events. To start, assess your individual needs by considering factors such as your current financial obligations, dependents, and long-term goals. It's essential to determine the amount of coverage needed by evaluating your existing debts, mortgage payments, and future expenses like your children’s education. By clearly defining these aspects, you can narrow down your options and avoid unnecessary coverage that could result in higher premiums.

Next, compare various policies by reviewing the terms and conditions offered by different insurance providers. Look for key features such as the duration of the term, renewal options, and premium costs. You may also want to check for any additional riders that can enhance your policy, such as accidental death benefits or critical illness coverage. To make an informed decision, it's wise to read customer reviews and consult with a financial advisor to find a policy that aligns with your unique circumstances and budget.