Understanding Whole Life Insurance: Benefits and Drawbacks

Whole life insurance is a type of permanent life insurance that provides coverage for the insured's entire lifetime, as long as premiums are paid. One of the primary benefits of whole life insurance is its cash value component, which allows policyholders to build savings over time. This cash value grows at a guaranteed rate and can be borrowed against or withdrawn, providing financial flexibility. Additionally, whole life insurance offers a fixed premium, ensuring that the cost of coverage does not increase as the insured ages. These features make whole life insurance an attractive option for those looking for a stable, long-term financial planning tool.

However, there are also notable drawbacks to consider when investing in whole life insurance. The premiums for these policies are generally higher than those for term life insurance, which can make them less accessible for some individuals. Furthermore, while the cash value accumulates over time, it typically grows at a slower rate compared to other investment options. It's essential for potential buyers to evaluate their financial goals and compare the costs and benefits to determine if whole life insurance aligns with their needs. Understanding whole life insurance allows individuals to make informed decisions about their financial future.

Is Whole Life Insurance the Right Choice for Your Financial Goals?

When it comes to planning for your financial future, understanding the role of whole life insurance is crucial. Unlike term life insurance, which provides coverage for a specific period, whole life insurance offers lifelong protection and builds cash value over time. This can be an attractive option for individuals looking to integrate life insurance into their broader financial strategy. By making informed decisions about your premiums and policy benefits, you can align your insurance choices with both short-term needs and long-term financial goals.

However, it’s essential to assess whether whole life insurance aligns with your specific financial objectives. Key factors to consider include your investment goals, risk tolerance, and the need for flexibility in your financial plan. While whole life insurance can serve as a stable and secure asset, it may not be the optimal choice for everyone. Weighing the benefits against the costs and exploring alternatives, such as term life or universal life policies, can help you make a decision that best suits your financial aspirations.

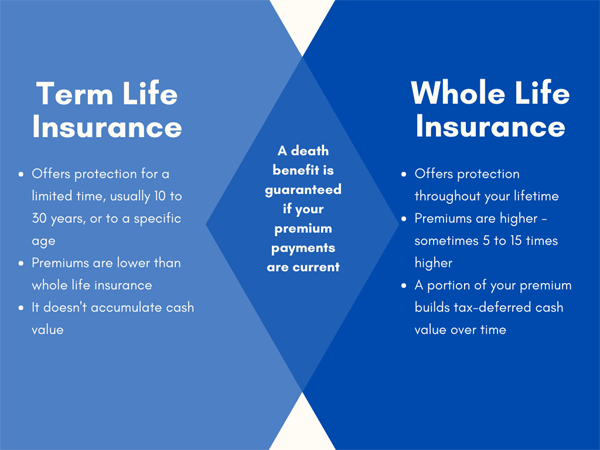

Whole Life Insurance vs. Term Life Insurance: Which is Better for You?

When considering Whole Life Insurance vs. Term Life Insurance, it's essential to understand the fundamental differences between the two. Whole Life Insurance offers lifelong coverage, which means your policy will remain in effect as long as you continue to pay the premiums. Additionally, it has a cash value component that grows over time, providing a potential source of savings. In contrast, Term Life Insurance is designed to provide coverage for a specific period, typically ranging from 10 to 30 years, making it a more affordable option for many families.

Determining which type of insurance is better for you largely depends on your personal circumstances and financial goals. If you seek an affordable premium and need coverage for a limited time—such as while raising children or paying off a mortgage—Term Life Insurance might be the ideal choice. However, if you desire lifelong protection and the potential for cash value accumulation, then Whole Life Insurance could suit your needs better. Assessing your goals, financial situation, and long-term plans can help you make an informed decision.